Succession planning is changing. Preparing for a family enterprise’s next generational transition has become more complex and challenging in recent years.

This is due to factors such as increased longevity, industry consolidation, a rise in M&A, evolving business models, and changing next gen career interests.”

In this live discussion, Prof. John Davis reflects on ways succession is being reshaped and answers audience questions about how families and owners need to approach succession with new insights for today’s changing dynamics.

Family enterprises that thrive across generations understand a critical truth: perpetuating a legacy does not mean preserving everything about it. Participants will learn the new definition of Stewardship: which is not about being a caretaker of everything you inherit — it is about actively shaping the enterprise to suit each generation, while preserving your edge for long-term success. This requires the discernment to know what to protect and what to renew.

Professor John Davis explores the owners’ dual responsibility to both perpetuate what makes the enterprise and family successful and adapt what must evolve to remain competitive and resilient.

Professor John Davis joins the YPO Brazil podcast “Extraordinary Leaders.”

In this exclusive episode, Prof. Davis shares his extensive experience and knowledge of the unique challenges and opportunities that surround family business management. Through an in-depth conversation, they explore topics such as the importance of planned succession, family dynamics in the business environment, and how businesses can thrive across generations.

In addition to practical tips for entrepreneurs and successors, Prof. Davis brings inspiring stories and valuable insights into leadership in the family context.

In this webinar, John Davis offers his insights for how owners lead effectively through turbulent times to build organizational resilience, maintain long-term enterprise performance, and sustain family enterprise success.

Times of turbulence—high volatility mixed with some disruptive change and high uncertainty about what’s next—demand even more from owners of companies. Even in relatively steady times, owners need to broadly guide their company and approve key changes (such as with investments and leadership).

In times like these, the importance of the owners’ role increases because more key decisions rise to the owners’ level.

Periods of volatility, disruption, and uncertainty require more from owners of family enterprises. Owners of family companies typically focus on strategic oversight and approving major decisions. During times of turbulence, owners need to let stakeholders know that “We are here to stay and we can manage this.

We have the vision, unity, agility, resilience, and resources to steer and guide the family enterprise and our family through these challenging, changing times.” In this webinar, Professor John Davis offers his insights for how owners can lead (as owners) through these times.

Watch this Webinar and:

Learn how the active owners of a family enterprise can lead through turbulent times.

Explore how governance needs to change to enable faster decision-making during periods of volatility and disruptive change.

Have the opportunity to ask Professor John Davis questions about challenges you are facing related to owning a family enterprise in these times.

MIT Sloan faculty John Davis and Deborah Ancona discuss why building an owners team is crucial, and what makes an owners team strong and effective.

Given the critical role and contribution of owners in the long-term success of a family enterprise, it is important that the owners remain a strong, unified, and capable team. This requires deliberate effort, especially over time and across generations as the ownership group grows larger and more diverse and complex. MIT Sloan faculty John Davis and Deborah Ancona will discuss why building an owners team is crucial, and what makes an owners team strong and effective.

Equip your family enterprise with the tools and knowledge to cultivate a united and resilient owners team for lasting success. Learn more from Davis and Ancona during their course: Future Family Enterprise: Sustaining Multigenerational Success Future Family Enterprise: Sustaining Multigenerational Success.

Key takeaways:

Why capable owners—especially active owners—are a key advantage for family businesses

The qualities of a strong ownership team and how they are developed

The challenges and practices of building a cross-generational team of owners in your family enterprise

In this webinar, MIT Sloan Professor John Davis explains how your family needs to excel at owner-level decisions—the most crucial capability for a family business to succeed in today’s turbulent environment.

Professor Davis is joined by third-generation family business owner, Karim Zahran, who will share his family’s story about the transformative power of an Owner’s Mindset in his family enterprise.

A podcast conversation with John Davis, Chairman and Founder of the Cambridge Family Enterprise Group and Senior Lecturer in Family Enterprise at MIT Sloan and Jason Jay, Senior Lecturer and Director of the Sustainability Initiative at the MIT Sloan School of Management. In this podcast, John and Jason discuss systemic investing.

In this podcast, Jason and John discuss Jason’s year of researching and discussing systemic investing with the FFI community.

The literature indicates that the board of directors exists to provide resources and strategic direction (service task) and monitor top managers (control task), often tending to overgeneralize board tasks. Using a unique sample of 36 elite family firm directors having served on 615 boards with an aggregate 1447 years’ experience, and integrating interview and secondary data with observations, we capture how the multiple role identity struggles experienced by family directors are managed in the board. Our data indicate that effective boards resolve multiple role identity struggles (i.e., family director ‘pathos’) through the mechanisms that boardroom structural forces trigger and the resulting bridge and buffer tasks enacted (i.e., board ‘ethos’), going beyond the traditional service and control tasks.

We have entered a new era that’s presenting unprecedented challenges, as well as significant opportunities, for family enterprises. Some of the traits of successful family businesses — their long-term outlook, strong financial resilience, stakeholder loyalty, and commitment to positive social impact — will aid their success in this new era. However, other traits — such as their insistence on privacy and control, their narrow definition of stewardship, their prioritization of family harmony over family unity, and their slowness in making big changes and reversing course — will need to change.

New mindsets, strategies, and practices will be required for family enterprises to survive and thrive in today’s turbulent era. Owners themselves must lead the charge, from the inside, and insist on new directions and transformative action to ensure success in the years ahead.

In a two-year study released in September 2022, sponsored by Citi Private Bank, Cambridge Family Enterprise Group (CFEG) explored these new requirements for success. Our research included a global survey of owning families, interviews with senior and next generation family members, and extensive secondary research — all guided by CFEG’s 33 years advising, educating, and researching family enterprises worldwide. The resulting white paper shares our learnings and advice for navigating the new era.

Having an owner’s mindset in today’s disruptive environment means excelling at making four types of owner-level decisions. All four are central to the long-term success of the family and its enterprise.

To remain competitive in today’s environment—one defined by disruption, borderless competition, rapid economic transitions, and constant technological transformation—families need to reconsider the way they own and lead their companies. Strategies that have remained reliable for centuries may no longer deliver results.

The traditional road to success

Family companies have historically focused on operational excellence. They have emphasized quality and steady improvements; aggressive reinvestment in their business; growing within their industry or in related areas; building loyalty among customers, employees, and suppliers; and choosing the right successor to lead the business. This has served family businesses well: when it comes to profitability, growth, and other performance measures, family companies have an impressive record of outperforming and outlasting their non-family competitors.

Traditionally, as family business have recognized the need for change, they have approached change slowly and circumspectly. They may acquire better equipment, work faster in some areas, improve processes somewhat, tinker with products and services, and promote talent as needed – but they make these changes incrementally with the goal of keeping things steady. This is an ownership and leadership style rooted in stability, tradition, and deep familiarity with a particular corner of the economy. It is informed by specialized knowledge and methods that have been passed down from generation to generation.

Professor John Davis of M.I.T. calls this approach to business the operators’ mindset. It has long suited family enterprises. But the reason such a mindset has worked is because industries and business models in the past have evolved slowly, over long periods of relative stability. Dramatic shifts or disruptions have occurred infrequently When change has been needed, adaptation could take place naturally, as the pace of the business world moved in step with families’ natural instinct to change slowly, wait for the right time, and obtain unanimous agreement.

We now, of course, live in a different world. Reliance on this approach alone appears to be a liability rather than an advantage.

The importance of an owner’s mindset

Success today requires blending the “operators’ mindset” with the owners’ mindset.

In contrast to operators, owners:

Gain altitude to take a high-level view of the trajectory of their businesses, industry, markets, competitors, assets, and family. They integrate plans across all of these considerations;

Move into growth opportunities by prioritizing value-creating activities and rejecting value-destroying activities sustained from old senses of loyalty, tradition, attachment, or conflict avoidance; and

Detach from businesses, investments, and people that aren’t working. Tradition and legacy are important, but they are not inviolable reasons to hang on to something that is no longer making—or in some cases even losing—money.

Families often have a particularly difficult time with this last one. Leaders who possess an operator’s mindset can be slow to recognize losing bets. They may be too attached to the business, to a tradition or legacy, or to specific people to admit that things need to change. Or, when they see problems, they think (in good operator’s style) that they can innovate their way out of the mess.

That should scare you, because if there is anything that families in business have to be good at in these disruptive times, it’s letting go of what isn’t working. This requires business leaders and owners to, first, clearly recognize when an investment has lost its momentum and, second, understand that they cannot necessarily make their bet succeed. When the problem before you is a changing industry trend, hanging on to practices that don’t work is foolhardy.

Industries are like a casino: you shouldn’t bet that you can outsmart important trends. You are unlikely to beat the house.

How to think like an owner

The mindset of active owners emphasizes long-term value creation through agility, entrepreneurial experimentation, and thoughtful diversification. It embraces new thinking, prudent consumption by the family and its company, and letting go of value-destroying and outdated activities in a timely way. These owners focus, most broadly, on growing and passing value in ways consistent with their values—whatever those may be. That is, the mission of the family enterprise from the owners’ perspective must be about growing and transmitting economic, social, and relational value while living by the values the family and enterprise determine are meaningful. We call this growing value through your values.

Having an owner’s mindset means excelling at making five types of owner-level decisions:

Setting the owners’ Strategic Vision for what they want to achieve and own with their jointly-held assets

Good bets on Capital Investments (including when to exit bad capital investment bets)

Good bets on key People (including when to change people in key roles)

Setting, protecting, and adjusting the Culture that is key to the family enterprise’s success

Designing the right Governance for the family enterprise so decision-making structures and processes are effective

All five are central to the long-term success of the family and its enterprise.

Some active owners are capable of having the mindset of both an operator and an owner at once. Others readily embody just one, which is fine as long as they appreciate the value of the other. What you must avoid in ownership groups is one mindset—usually the operators’ mindset—becoming the religion of the group. When some owners or advisors point out that the industry is maturing or being disrupted, and the family business can’t succeed in such an environment, and that maybe, just maybe, it’s time to sell the family business and invest in new growth areas, they shouldn’t be branded as heretics. Owners need to appreciate the value of both perspectives.

Build a team to represent both mindsets

Ultimately, both mindsets—operator and owner—help to cultivate the success and sustainability of the family and its assets. Good owners do not neglect operational excellence by any means, but rather delegate operational excellence to a capable management team (whether family, non-family, or both). Owners need to embed the family’s values within the company; they need to arm managers with the owners’ vision and the board’s approved strategy, and let them operate. Charge them with designing better products and processes then step out of the way and work to solve owner-related challenges.

For example, as noted above, big bets on investments and on high-level talent recruitment often rise to the level of the owners for input or decision. Should we take on more debt, bring on an investor, or go public? Should we sell a particular line of business or the whole company? Should we enter this new industry? Should the next CEO be a family member or non-family? Counsel from the board and other advisors is useful for informing such owner-level decisions, but the final choice ultimately lands with the family owners.

To achieve parity between these two mindsets, families should establish forums where owner-level issues and important owners’ goals can be discussed, owner-level policies decided, and new directions set. One way to do this is an owners’ council. Also, under the right circumstances, a portfolio board that recommends portfolio strategy is useful. Independent advisors on boards and elsewhere are a third resource for assuring an owners’ mindset has room to guide the company and family assets. In short, give yourselves permission to think like owners by structuring regular owner-centered conversations.

In disruptive times, it is owner-level decisions that often make or break a business. And it is precisely these types of decisions that demand an owner’s mindset. Without taking steps to establish and reinforce an owners’ mindset at the top of your family enterprise, the past epoch of success may become nothing more than that—something of the past.

Making Family Councils More Effective A 4-day, Interactive Workshop on Family Governance for Tomorrow’s World

This LIVE event took place, October 5-8, 2020

In a series of live, online sessions over four days, Family Council leaders and members from family enterprises across the world gather to explore how Family Councils must adapt to add strategic value in today’s disruptive world.

Active participation is required. Sessions include live, interactive presentations by faculty, daily working sessions in small workgroups, self-reflection and analysis of your own Family Council, and active dialogue and support among participants and faculty.

PROGRAM SUMMARY

We have entered a new age for enterprising families – A new age that calls for Family Councils to elevate their support of the family and its enterprise. It is time for Family Councils to take an active, strategic role in preparing the family for the bold moves that will keep the family and its enterprise adaptive and successful in the New Economy and New Society.

In today’s complex world, family governance is more needed than ever but must adapt to stay effective.

How does a Family Council pivotally help the family to stay united and decisive, build key talent, and support its enterprise?

How do Family Councils need to adapt to add strategic value in today’s disruptive world?

Join us for an advanced program for mature Family Councils to explore how to elevate the Family Council’s strategic support of the family and its enterprise, and prepare the family for tomorrow’s world.

The Covid-19 crisis is a time when you should gauge your family’s resilience—and build more of it. An enterprising family’s goal is to not just cope with adversity, but grow stronger as a result of it. Here are ways to achieve that.

The Covid-19 pandemic is a huge, disruptive event that is severely challenging every aspect of our societies, every level of our governments, and all sectors of our economies. This pandemic is a disorienting, strongly felt shock to our collective nervous system—a textbook case of a major crisis and setback. The health, societal, and economic upset from this disruption will rumble through the world for the rest of this year and into the next. The human, economic, and social costs of the pandemic are staggering, and the ultimate costs are only now being imagined. Some businesses will prosper during this period, but most will struggle, and no economy will be spared.

What will be the impact of the crisis on enterprising families?

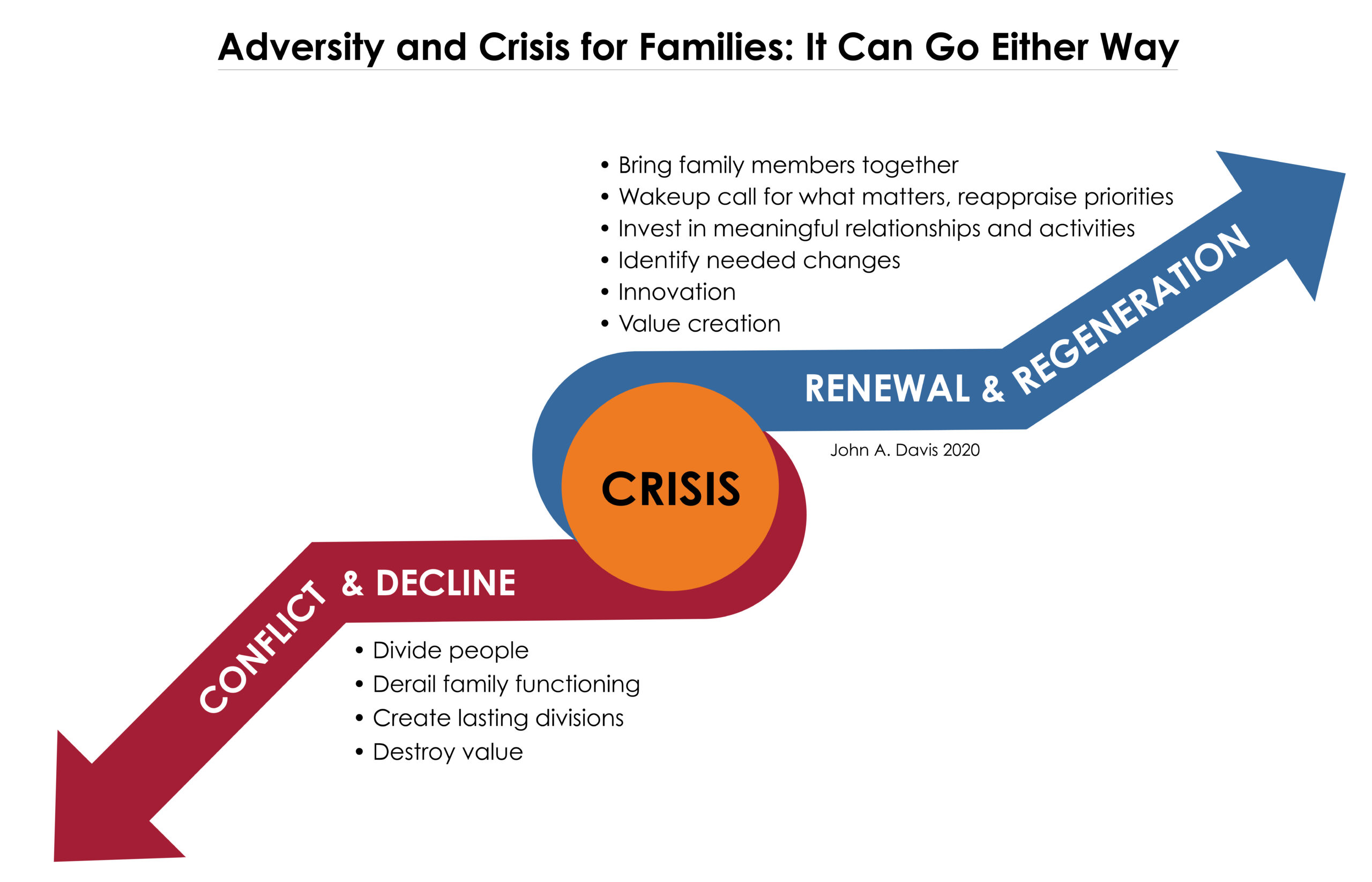

There Are Two Possible Outcomes for a Family

Adversity and crisis can either lead a family and its enterprise into decline, or into renewal and regeneration. It can go either way.

If you are not resilient, a crisis or prolonged adversity can more likely divide family members, derail family functioning and decision making, create lasting divisions, and destroy value.

If you are resilient, adversity will more often bring family members together, be a wakeup call for things that need to change, motivate more attention to meaningful relationships and activities, bring innovation to systems, and lead to reinvention and value creation.

Causes of Family Derailment

It’s easy to understand how crisis situations or periods of prolonged adversity can cause families or other groups to have difficulties. Crisis situations like we are in now can easily produce these outcomes:

Family members can feel considerable anxiety about their circumstances.

Some anxiety is needed to respond well to problems but too much anxiety paralyzes us or makes us aggressive. Great anxiety usually leads to more emotionally-reactive and self-protective behavior, and it is often associated with a loss of confidence, hiding from problems, rushing and staying busy but not solving critical problems, and looking for magic bullets, while tending to see a narrower scope of options. If you see these behaviors, as a leader you need to calmly but directly address them: reassure group members that these behaviors are understandable but not helpful or acceptable, and refocus family members on solving specific problems together.

Family members can experience loss and, understandably, fear that they will experience more loss.

People are experiencing a range of losses in this crisis–the loss of loved ones, of course, being the most profound. But it is not the only one: financial losses, loss of employment and income, loss of opportunities, loss of social interaction, loss of normalcy, loss of predictability, loss of control. Losses during this adverse time can raise old issues to the surface that can no longer be ignored. (In good times, money has a way of concealing problems.)

Typically, there are new crisis issues to manage that we may not be familiar with or feel capable to handle.

The combination of old and new issues can lead family members to feel a loss of control, resulting in the tendency to blame others. This results in conflicts, instead of pulling together.

The Key Determinant is Resilience

The key determinant of decline or regeneration (besides external forces and luck) is the presence or not of resilience in a group.

Resilience is the capability of an individual or group to get through and recover well from prolonged adversity, important setbacks, or crises. Resilience is created by having adequate resources, useful structures to support the family and make key decisions, and trusted leadership.

Think of resilience as a storehouse of these three types of ingredients:

Resources

material resources to help cope with loss and maintain stability

skills that are useful in a crisis or in a period of prolonged adversity (e.g. composure, courage, perseverance)

experience solving tough problems while keeping members of your group united

allies, advisors and friends who will help in a crisis

a strong sense of purpose, trust, and pride in our family

willpower and sense of hope to get through adversity, recover, and move forward again

unity of family members, especially under pressure and conditions of deprivation

family members who care for others, encourage them, and help them cope with loss

Leadership

trusted leadership who can make wise, fair, tough decisions

a leader who focuses our attention on needed accomplishments and encourages collaboration and problem solving

a leader who conveys hope and purpose (why is it important to get through this)

Structures: Roles, Forums, Agreements, and Decision Processes

clear roles for who decides, who is consulted, and who is informed of key information

forums (like boards, family councils, owners’ councils) where groups can have important conversations and make key decisions

decision rules, principles, and processes that help build consensus and help us make tough decisions

ownership agreements and family policies that help maintain the stability of the group in hard times

>> I encourage you to do a quick assessment of the presence of each of these resilience ingredients in both your family and your family company.

Each of these resilience ingredients lowers anxiety in stressful times, encourages collaboration, and allows us to focus on important problems to be solved. Success through a crisis requires that these resilience ingredients work together to overcome hardship and achieve recovery.

Ideally, you should strengthen as many of these factors as you can before a crisis and be ready to re-energize any of these that weaken in adverse times. The weakest link in our arsenal (say, trust in other family members) can become overstressed and fray in hard times, then can stress other factors (like family unity and our material resources), which can further stress the system and eventually bring us down. System failures are usually the result of cascading and compounding smaller failures.

Resilience is Needed Today More than Ever

Around 2000, we entered a new age, which is ushering in more frequent and more volatile disruptions to industries, societies, companies, and families. It is common to describe today’s environment, borrowing from military parlance, as VUCA: Volatile, Uncertain, Complex, and Ambiguous.

Accelerating changes in technology along with increased globalization has reshaped how commerce is done. Industries are changing, maturing, and disappearing much more quickly. Society is experiencing shifts such as increased diversity, increasing transparency, greater digital connectedness, and more political disruptions and social tensions. Scientific breakthroughs are increasing human lifespan and changing former genetic limitations. Business families themselves are morphing, becoming more diverse, more geographically dispersed, more international, and more egalitarian. The Millennials are changing the ways in which we do business, care for the world, and lead our lives. Add to these factors that societies, companies, and families must cope with periodic, widespread disruption such as the tragic Covid-19 pandemic.

In these conditions, companies must innovate constantly, anticipate disruption, and consider wider diversification to stay alive. The families behind these companies must themselves be innovative, agile, and resilient.

Resilient families and companies that get through the Coronavirus crisis will need then to get ready for the next disruption, and the next, because further disruptions are coming. Companies have heard this admonition for at least a decade, and progressive companies now consider how they can become more resilient and hopefully disruption-proof. A good part of my work today is helping family companies, family offices, and their owning families become better prepared for this new age, including growing more resilient.

Why Family Resilience?

We definitely need to build the resilience of the enterprising families behind family companies and family offices. The family is the ultimate foundation for a family enterprise—even more fundamental than the family owners.

FOUNDATIONS FOR LONG-TERM FAMILY BUSINESS SUCCESS

The ability of a family business to survive long-term depends greatly on the ability of the family to:

stay united, decisive, and industrious

make important directional decisions for its business(es) and assets

produce enough family talent to contribute in key ways to the family enterprise (e.g. as owners, wealth creators, board members, governance members, and in other ways)

support adequate reinvestment in the company.

If your family is not resilient, it will likely undermine the resilience of your ownership group and then your enterprise.

The good news is that a family and company that are able to successfully move through serious adversity will likely be better prepared for the next disruption. The family’s confidence, judgment, skills, unity, and pride will be strengthened and become embedded in its memory, giving the family or company a better chance to overcome the next setback it faces.

Help Your Family Develop Resilience

How resilient is your family? How does your family deal with prolonged adversity, setbacks or crisis? What are you doing to help your family learn from this period and grow in capability?

Your family’s goal should be not to just cope with the adversity it faces, but to grow stronger as a result of it. Your objective is that strengths come out of this struggle.

How do you achieve that? A family can build and reinforce resilience in good times and also during a crisis. In the midst of the current crisis, these actions will help:

A family grows stronger as a unit by pulling together toward a common goal, supporting one another, and collaboratively problem-solving through hard times. Set previous disagreements aside. Don’t let them divide you in these times.

Family leaders need to actively shepherd the family through this crisis: be open with the family about the challenges the family and its company face, give hope that both company and family will make it through this time, focus the family on specific concrete goals and actions, and stress the need for trust and collaboration.

As much as you need strong performance during this time, emphasize the importance of behaving according to core family values. A family will be proud not just because it survived a crisis, but because it survived the crisis while keeping its values.

Families need to know what, besides saving the family’s fortune, the family should try to accomplish in this crisis. Define what your family wants to protect and what its big goals are. Be open in this time to redefining how you achieve success as a family.

Praise teamwork and support collaboration among family members. Challenge any attempts by some to achieve political advantage of the crisis for one faction or another in the family.

Be a role model for future generations. An individual, a generation of the family, or the whole family can be a good role model for future generations regarding overcoming a crisis. Resilience is transmitted through the generations not only through successfully rebounding from adversity but also through role models. You learn from role models who acted bravely in crisis periods; they become memories that you will recall when you’re experiencing future challenges.

Resilience Builds on Itself

Getting through tough situations together as a family helps build the confidence, trust, pride, relationships, unity, and skills to face new challenges and rebound from the next crisis. Resilience builds on itself. It’s a virtuous cycle.

Which of the family resilience ingredients are abundant in your family? How are you reinforcing them?

Which of the resilience ingredients are in short supply in your family? How can this crisis aggravate your weaknesses?

STRENGTHEN YOUR FAMILY’S RESILIENCE

Which resilience ingredients can your family try to develop during the crisis?

How can you organize your family to pull together in this crisis?

How are family leaders guiding and focusing the family on getting through the crisis?

Which of your family’s core values are you demonstrating and reinforcing in your crisis response?

What are your family’s big goals to achieve in this crisis? Are you discussing these goals as a family?

How well is your family supporting and championing one another and collaborating constructively to solve problems?

Are you creating role models for future generations to learn how to navigate a crisis and rebound from it?

Is the senior generation in your family talking with the next generation about how they’re approaching the crisis and what it takes to get through a tough period?

With an appreciative nod to Gabriel García Márquez and his literary classic, Love in the Time of Cholera. García Márquez teaches us all the value of persistence and resilience.

The performance edge family businesses have over their non-family business counterparts has been explained by their dogged pursuit of operational excellence. Family firms tend to take a long-term view of investments and relationships, stay in ownership control to do things their way, focus on persistent improvement and innovation, develop loyal stakeholder relationships, build key talent in select individuals, carry lower debt, and build greater financial stability. This approach to running a business reflects an Operator’s Mindset. It is informed by specialized knowledge passed down from generation to generation. This mindset is deeply embedded in the cultures of most family companies and business families: If you want to be important in the company and family, you have to be good at operations.

Cultivating an Operator’s Mindset has largely paid off because most industries and business models have, until recently, evolved slowly, making operations quality central to success. But dramatic shifts do happen and, when they do, family companies that can’t think beyond the Operator’s Mindset often fall behind.

Family companies that have persisted over generations despite changing conditions strive for operational excellence, but not exclusively. They also are skilled at migrating to new value-creating activities and at leaving activities and practices that destroy value. They don’t become stuck in traditional businesses or outmoded practices. Some, after exhausting growth opportunities in their core business, diversified into different industries. Some experienced their industry maturing and consolidating around them and decided either to stay and acquire competitors or sell their outflanked business and redeploy assets. Some have parried the disruption of technology or regulation. Such adaptations are profoundly informative.

What distinguishes these long-term adapters is their strong Owner’s Mindset among the owners and in their top boards. An Owner’s Mindset recognizes the importance of operational excellence, but insists on being in activities that create value (financial, social, relational, and reputational) according to the key values of the owners.

Davis leads you on a personal and professional voyage back to the 1970s to pay special homage to the groundbreaking work of his late mentor, Renato Tagiuri, who pioneered the field of family business with frameworks that included their notable Three-Circle Model of the Family Business System.

Davis then pivots to the future and offers a modern roadmap for business families to transform themselves to conquer the next economy. FBN invites you to partake in the new paradigm of business families leading the sustainable change required to address the great challenges of our time.

Looking into the Future of Business Families overflows with poignant lessons and forward-looking tools for multigenerational families, researchers, professional advisors, and the entire ecosystem of the family enterprise field.

The book launched at FBN’s 30th Global Summit in October 2019 in commemoration of FBN’s 30th anniversary. The book will be widely released in Q1 2020.

Is your family growing the value you want to be building?

Learn from MIT’s family enterprise experts about the two latest trends that help families build value (of various kinds) across generations, particularly in this era of rapid change and global uncertainty.

MIT Sloan faculty John Davis and Jason Jay discuss their latest insights on two emerging trends: how an owner strategy and systemic investing are being put to use by families to grow value, develop family talent, and build family unity across generations.

This webinar is especially relevant for the owners and leaders of family enterprises and family offices who want to stay ahead of the curve and gain new insights about family enterprise success.

Key takeaways include:

Why family enterprises need to pivot their value-creation strategies, given today’s turbulence

How families are putting to use two strategies to build value: an owner strategy and systemic investing

How your family can make use of these strategies in your family enterprise or family office

The latest thinking on family enterprise out of MIT

Information about the upcoming Future Family Enterprise program

Today, family business leaders and owners face some of the most challenging and high-stakes decisions seen in a generation.

How are YOU navigating the complex decisions that your family enterprise faces? Let’s dig into them together in this important conversation—a Q&A with Professor John Davis.

Featuring Professor John Davis of MIT Executive Education

Family enterprises face big challenges in order to survive and thrive in our era of rapid technological and market disruption. Having to adopt to new business models, and accept changing customer loyalties, they must also address changing attitudes and aspirations within the family itself, as the Millennial generation takes the reins of the family business.

The Millennial generation (Gen Y) is, arguably, the most researched generation in history. The subgroup of Millennials from business families has not been well understood until Professor John Davis’ recent study of business family Millennials from more than 40 countries.

Following his highly popular 2019 webinar, IEDP welcomes back renowned academic and shaper of the family enterprise field, MIT Sloan Professor John Davis, to share his latest research findings about Millennials’ interests and aspirations for their lives, careers, financial wealth, and their family business.

In this Trusted Family Webinar, Professor John A. Davis discusses the Three-Circle Model in-depth. The webinar explores the history of the Three-Circle Model and answers many questions, including which group has the most power in the Model and does the Model now need a 4th circle?

MIT Management Executive Education November 15, 2021

This is a new era for family businesses. To succeed in this turbulent period, family businesses must adopt new practices at not only the operations level, but also at the ownership level.

Professor John Davis explores the owner perspective, owner-level decisions, and how to architect governance to make these strategic decisions for the family business and family assets.