Trusted Family Webinar

January 17, 2019

In this webinar, Professor John A. Davis explores some current trends in corporate governance and discusses how to ensure a high-functioning board for a family business.

.

Trusted Family Webinar

January 17, 2019

In this webinar, Professor John A. Davis explores some current trends in corporate governance and discusses how to ensure a high-functioning board for a family business.

.

WealthManagement.com, by Mitzi Perdue, February 26, 2019

Professor John Davis is one of the world’s leading authorities on family enterprises. How would he advise business families and their advisors to prepare for a world of ever-more-rapid technological change?

Davis has advised multi-generational family enterprises in more than 65 countries. His professional training includes management, psychology and economics. He’s also spent decades teaching at the Harvard Business School and currently leads the family enterprise programs at the MIT Sloan School of Management.

John Davis: The workforce of the future will look quite different than it does today. Not only are existing jobs being threatened, but new jobs will emerge that don’t exist today. A combination of reskilling and upskilling is going to be important in order for talent to keep pace with innovation.

While there are many more skills required than these, below are four important categories that will be increasingly needed in the next economy:

JD: I moved to the faculty at MIT because of its focus on the future. MIT is way ahead of other schools’ understanding of what’s happening and changing in our world. In many ways, the MIT ecosystem—with its many labs—is creating the Fourth Industrial Revolution that we’re all preparing for.

My work at MIT focuses on helping family enterprises prepare for the ways in which the future will impact them—and there are many. There are forces affecting businesses, families, ownership, investing, philanthropy, governance, talent and virtually every aspect of a family enterprise. Technology is only one force we hear about a lot, but there are others that I’m paying close attention to and helping families prepare for.

JD: In addition to technology, I am watching social and demographic changes, the rise of the Millennial generation, globalization trends, industry disruptions, environmental shifts, political movements, the actions of governments, and other forces. These are opening up opportunities for families, giving rise to some challenges, and revealing the need to adapt, which is not so easy.

Family enterprises are inherently wired for stable or gradually changing environments, because gradual change is more compatible with family culture. Most enterprising families aren’t wired to flex with substantial change, fast change or disruptive change (although some do this admirably). Family companies generally do well with managing economic cycles, but industry disruptions, which happen more frequently than economic cycles, can have more profound impacts on a company or industry, and family companies need to build new practices for the new business world. Enterprising families need to:

JD: I’ve launched two programs at MIT in 2019 (Future Family Enterprise, May 5-10, and Founder to Family, July 22-26) to help families at specific stages in the life cycle learn to succeed in new ways with new mindsets. I invite families who want to learn about these experiences to be in touch with me at [email protected].

Mitzi Perdue is a professional public speaker and author of the book, HOW TO MAKE YOUR FAMILY BUSINESS LAST a Treasury of Checklists, Templates, Resources, and Tips. Visit her website, www.MitziPerdue.com.

MIT Sloan Executive Education faculty member John Davis, a pioneer in the study of family companies and the director of MIT Sloan’s portfolio of Family Enterprise Programs, is bemused by the sudden interest of corporations in ‘long termism’. “We see non-family, publicly-traded companies suddenly ‘discovering’ long-termism— as if they really discovered it. I’m glad they’re thinking about it; let’s see if they make a genuine effort and really do it,” he says.

Davis remains skeptical—and for good reason. He knows long-termism well, and he knows it works. He teaches the practices, planning, and mindsets to do it successfully to classrooms of business families at MIT. For more than 40 years, across 70 countries, Davis has studied, taught, and advised family-owned companies on how to survive in business for generations. What amuses him about Wall Street’s recent appeal for long-termism is that they define “long-term” in many cases as three years. Meanwhile, Davis works on 25-year, 50-year, and 100-year plans with multigenerational families, and was recently asked by a founder to develop a plan for his family enterprise to last 500 years (20 generations).

Family companies, Davis believes, favor the decisions and behaviors that matter to long-term, sustainable performance “more naturally and more inherently than non-family companies.”

Date: May 3–8, 2020 │ Format: In-class study with action-planning │ Location: MIT Campus, Cambridge, MA

Long-term thinking has always been at the heart of successful family companies. “And not only long-term thinking, but also planning, investing, partnering, relationship-building, and community-building for the long-term,” Davis explains. A long-term perspective “comes more naturally inside a company that is owned by a family, because their time horizon is intrinsically longer. They plan for their descendants to own this business or this land (or the wealth generated by its sale) for generations. There is an attitude of legacy and stewardship as a way of being in families, which permeates into the culture of the company.”

Another inherent quality of a family that penetrates the family company is the stability of ownership, “which says that what we’re in this for the long haul – it’s not a speculative venture – and if you come to work for us, or if you’re one of our customers or suppliers, we’re sticking this out.” This is reflective of their fierce loyalty, which “family companies tend to nurture more than non-family companies.” Davis cites.

Family companies also tend to develop financial stability, with stronger balance sheets and less debt. This makes them more resilient to economic downturns, avoiding the frantic efforts many non-family companies make to boost their suddenly shaky bottom lines. Davis’ work at MIT now focuses on how family enterprises can survive today’s disruptive, fast-changing environment, which requires some different skills than outlasting economic cycles.

The qualities described above that are inherent to family companies help explain one of the business world’s best-kept secrets: on average, family companies, whether public or private, whether small or large, consistently outperform their non-family counterparts. As established by the research, the difference in profitability, growth, or any other kind of return is significant, he says. “We’re not saying that all family companies perform better than all non-family companies,” Davis notes, “but on average, they do.”

Most industry leaders are family companies. The majority of publicly listed companies are family controlled. While the famous three-generation rule – which states that many family companies don’t survive past the third generation after founding – may have some validity (Davis has researched this), the fact is that even fewer non-family companies ever last three generations.

Of course, family companies have their challenges as well. One of the main vulnerabilities of family companies is their reluctance to “let go.” As Davis explains, “Family companies hold onto people who aren’t working out well way too long, they hold onto investment bets that aren’t working well too long, they hang onto products or business lines that aren’t working well too long, and sometimes the senior generation hangs on to leadership too long. Families tend to be excessively loyal, stubborn, and they get attached. That doesn’t work very well in today’s economy.”

Date: November 9–13, 2020 | Format: In-class study with action planning | Location: MIT Campus, Cambridge, MA

The irony is that by remaining loyal to original products or to the original business rather than experimenting and scanning the horizon for new growth opportunities, the younger generation of a business family forgets the spirit that inspired the company’s founding in the first place. The driving ambition of the company’s founder was “to create something new that people will value,” says Davis; building a company was only the means to that end. Later generations, however, get attached to the means and forget the ends. As Davis urges his family company students and clients, “We need to migrate to new, good opportunities, and not fixate on the means of production.”

The challenge is that families have a passion for the family business, which is both a strength and a vulnerability. “It’s hard to create anything of great value if you’re not passionate about it,” Davis says, “but passion for a business also results in attachment to it.” Davis, who is also a trained psychologist, notes that success in life often depends on the quality of our attachments but also on our ability for detachment. Successful parenting, for example, requires balancing attachment, and, as children grow older, detachment.

At the family company level, achieving this balancing is a part of the culture that is set in motion by the owners, and then filters into the board and organization, says Davis. “How do you balance attaching and being passionate about something, but also moving away from it at the right time and letting go of things that don’t work any longer?” According to Davis, this skill is an essential part of the modern success formula for family enterprises in today’s turbulent environment. Most family owners don’t know how to do it well; they congregate in Davis’ classes to learn how.

The best family companies know when to pivot and divest, but they also work hard to ensure that such moves are achieved in a positive and humane manner. “When a family business shuts down an operation in a community and people’s lives are affected, you are judged rightfully about how you treat the people who helped you over so many years,” says Davis.

“Good families and good family companies make the right moves in the interest of long-term value building, but they do it with the right values,” he says. “They treat people with dignity, they help them find new jobs, they help the community, maybe repurpose their old factory in some way. They honor contribution and loyalty–and their roots.”

Such timeless values will ensure that no matter how volatile, chaotic, and uncertain the world around them, the best family companies will continue to quietly outperform their noisier, short-term focused, non-family competitors.

Learn more about MIT Executive Education’s portfolio of family business programs here

Ideas that Matter MIT Sloan, 2019

Walmart, Comcast, Nordstrom, BMW, Ikea, Zara, Lego, Samsung — all multibillion-dollar empires, all family companies. These companies testify to the power of the family business model, in which ownership is controlled by a single-family and two or more family members significantly influence the direction of the business through management or governance roles, ownership rights, or family relationships. Most of the world’s businesses, in fact — including many of the largest ones, even among those that are publicly traded — are family companies.

While family companies can be superior performers and leaders in innovation, all forms of enterprise have their weaknesses. One vulnerability of family companies concerns the transition of ownership and leadership between generations. Most of these transitions are not managed well enough and too many end in failure for the company and family. This is especially true of the transition between the founder and next generation, but this vulnerability persists in any generation of family control.

All this is according to John Davis, a senior lecturer in the MIT Sloan Executive Education family enterprise programs. Davis has spent four decades studying, teaching, and advising family-owned enterprises on how to sustain their success over the long term, including the pivotal transition of leadership from the senior generation to the next. Davis offers key guidelines for family businesses that are facing a shift between generations. While each generational transition presents distinctive challenges, these four management principles apply universally.

Maintain momentum

Momentum, or forward movement of a business or family, “is an underappreciated force that we need to be very respectful of,” Davis said. “If you kill, stall out, or even significantly reduce the momentum in a system, it’s hard to make it up.” Families need to steadily grow their financial assets, develop talent for the whole enterprise, and maintain group unity to stay ahead of company, family office, and family-related challenges.

Maintaining momentum must include preparing for and willfully making a transition from one generation of ownership, governance, and leadership to the next. Steady progress towards the goal of a successful handoff is a far better strategy than ignoring preparation and taking your chances at the end of a generation. Davis likened this to handing off a baton in a relay race: Both generations need to be running at the same speed for a smooth pass.

You need to pass the baton when the next generation is ready to lead — not when you’re ready to leave.

This analogy nicely captures the importance of timing. Transition from one generation to the next too soon and you will likely stumble. Delay the transition too long, and the next generation may be detached from and uninterested in the work. Growth can stagnate. Morale and unity can crash. According to Davis, the right timing hinges on one central consideration: “You need to pass the baton when the next generation is ready to lead — not when the senior generation is ready to leave,” Davis said. “And that’s an understandably tough principle to expect the senior generation to champion.”

No company head or leader of any enterprise organization, especially a founder with a deep personal investment in the company or family office, wants to leave “the game” that they are good at and enjoy playing, Davis said. To facilitate timely transitions, leaders need to plan for their next chapter of life and families need to identify valued roles for elder family members.

Question the ‘theory of one’

“A generation transition involves a passing of ultimate responsibility for all of the major activities of the family,” Davis said. “This almost always involves passing the leadership of the family company, but families have more interests than just the family company.” Consider philanthropy, the family office, the management of the family’s outside assets, and the leadership of the family itself. At the end of the process, you want a capable and committed next generation successfully leading the family’s key activities.

Many families believe all of these activities can and should be led by one person — the “theory of one.”

“Sometimes this approach works, but it has consequences: It not only saddles one person with wide responsibilities, but often means some family activities will get little attention, and that only business leadership will be valued,” Davis said. “There are better ways for a family to get things done and maintain unity.”

Smart transitions are about having a team of family members (and non-family managers where appropriate) ready to take on different positions and responsibilities in the future.

Prepare the business (and other family organizations) for the transition

Maintaining momentum also means that companies need to be prepared to support and flex with the changes the next generation brings. “That means preparing for new investments in new business opportunities, reconsidering standard management practices, strengthening the company’s balance sheet, adapting the culture of the company, transitioning key customer relationships, and so on,” Davis said. “You want the next team to hit the ground running.”

The new generation of leaders will hopefully want to pursue some different strategic goals and, likely, will manage with a different style. The senior generation and the organization must integrate and facilitate these changes while maintaining important corporate values — without starting a tug of war between entrenched practices and the new vision. “It’s typical for the senior leaders to see some change as threatening, rather than exciting, and for next gens to feel held back,” Davis said. “But transitions go better when the next generation shows appreciation for the accomplishments of the senior generation, and the senior generation appreciates the need to change in healthy ways.”

Build a new ownership team

In a generational transition, ownership is generally passed from a smaller to a larger group of people and a new group of owners must support the business and other activities of the family. According to Davis, ownership should be treated like a job — a strategic tool — but most families spend little time considering who deserves to be an owner and how ownership should be structured. “Families are generally on autopilot regarding the ownership transition,” he said.

Instead, the two generations need to have transparent conversations about how ownership will be exercised, divided, and transitioned. What is the job description for family owners or beneficiaries? Should shares be passed over a 20-year period starting when the next generation of owners is in their 30s? Should ownership be given to individuals based on specific conditions, such as being an employee? What kind of shareholder agreement will best serve the next generation? The right kind of ownership formula will provide a more stable foundation for the business organization and build unity among the succeeding generation. The next generation of owners must not only be well-prepared individually to perform as owners but need to be trained and motivated to coordinate like a team.

Of particular concern are situations where ownership is only passed, or even revealed, when the senior generation dies. “This is dangerous,” Davis said, “and not simply because of estate taxation. When ownership comes all at once, at an emotional time, the next generation is unpracticed as an ownership team.”

The Family Business Podcast

December 7, 2018

In this episode, John Davis discusses Disruption and Innovation, and how they are changing the lives of family enterprises and the families that own them. He explores ways that family enterprises are in motion, and how they must adapt to today’s accelerated pace of change. After all, disruption provides an opportunity to pivot and embrace experimentation. He offers family owners—in the senior generation and next generation—useful advice for responding to disruption and partnering together through this new global disorder.

You may also be interested in John Davis’ article The Owners’ Mindset in the Age of Disruption

Cambridge Family Enterprise Group

October 9, 2018

Professor John Davis, co-creator of the Three-Circle Model of the Family Business System, Professor John Davis, co-creator of the Three-Circle Model of the Family Business System, describes how to build highly effective groups in the family business system.

ame>

Cambridge Family Enterprise Group

October 9, 2018

Professor John Davis, co-creator of the Three-Circle Model of the Family Business System, describes how the model can be used to help build unity in the family business system. He discusses the three ingredients required to sustain family success: GROWTH of Family Assets; Family and Organization UNITY; and Family and Non-Family TALENT.

Cambridge Family Enterprise Group

October 9, 2018

Professor John Davis, co-creator of the Three-Circle Model of the Family Business System, describes what the Late Renato Tagiuri would think about the 40th anniversary. “My colleague and friend, Renato Tagiuri, would be delighted and probably a bit surprised, at least amused, that this little conceptual tool that he and I created out of necessity to understand family business systems has been so successful for so long.”

Cambridge Family Enterprise Group

September 26, 2018

Professor John Davis, co-creator of the Three-Circle Model of the Family Business System, describes how the model can be used for succession planning. Learn More >

Trusted Family Webinar

August 2, 2018

John A. Davis, Founder of CFEG and Faculty Director, Family Enterprise Programs, MIT Sloan School of Management discusses understanding disruption and its impact from the owner’s perspectives with Edouard Thijssen, Co-founder and CEO of Trusted Family.

The Family Business Podcast

July 20, 2018

In this episode, John Davis has a rich discussion with host, Russ Haworth, on the occasion of the 40-year anniversary of the Three-Circle Model of the Family Business System. He describes how the Model can be used by families and their advisors, and reflects back on how he created the Model in 1978 with Professor Renato Tagiuri at Harvard Business School. The conversation expands to delve into some future trends that John Davis sees on the horizon for family businesses.

You may also be interested in John Davis’ article How the Three Circles Changed the Way We Understand Family Business

Cambridge Family Enterprise Group

July, 2018

Professor John Davis, co-creator of the Three-Circle Model of the Family Business System, describes how he and Professor Renato Tagiuri created this groundbreaking framework. Today it continues to be the most widely accepted, organizing framework used worldwide to understand. Learn More >

Cambridge Family Enterprise Group

July, 2018

Hear what John Davis has to say about the Three-Circle Model. Should a Fourth Circle be added?

FFI | Practitioner – June 13, 2018

This week’s FFI Practitioner concludes our two-part series commemorating the 40th anniversary of the influential Three-Circle Model. Thank you to FFI Fellows, Pramodita Sharma and John Davis for sharing their insightful conversation about the future of the model, research, and the field. Read the Full Article >

Pramodita Sharma (PS): As I walked into my office for our interview, I ran into one of our Sustainable Innovation MBA students. They are reading my book Entrepreneurs in Every Generation, so I asked: “How’s my course going for your class?” And she said – “Honestly, you know what? I love the three-circle model. It applies everywhere, in every course.”

Her comment made me think perhaps we should use the three-circle model in our PhD programs, because if you think about the theories we refer to, e.g., agency theory, resource-based theory, we can go back to the three circle regions and say, OK, where does a theory like agency theory fall in the three circles? What issues of the three-circle model are we trying to address with it? The three-circle model is the starting place to understand these systems. I really believe the model’s impact is only now beginning to show. When I put the three-circle model on the board, people can use it to think in a theoretical way, as well as locate themselves in the model as practitioners.

In my case, teaching, for example, most of the variants that you’re trying to capture in a case and to get people to talk about having to do with the seven regions in the three circles. It’s not as if it’s all we talk about, but after people have used the three-circle model in traditional ways, they try to use it to explore other issues. For instance, the implications of wealth in the business, or in the family, or both. It seems like there is no question that we’re talking about another dimension. Can you, or did you ever, imagine positioning a wealth circle?

John Davis (JD): First, it’s gratifying to hear that your students and you think the three-circle model is useful theoretically and managerially. That never fails to buoy me. I agree that the model is a foundation for understanding the family business system. Other theories like agency theory can be understood in the context of the three-circle model. Unfortunately, and not to get distracted here, but it’s disappointing that some reviewers for journal articles I have submitted recently see “no relevance” for the three-circle model. Seriously? While you, a highly respected researcher and theoretician, are deeply understanding of family business system issues and appreciative of the power of those three little circles, other academics in the field are not.

But I am the first to recognize that the three-circle model is not designed to answer all important questions in our field. No framework can. Take the interesting topic of family wealth. While every family owner of a family business is a wealth holder, a family’s wealth includes assets outside the family business, and some family members could be a holder of some family wealth and not an owner of the family business. Believe me, I have played with adding a fourth wealth circle and couldn’t make it work conceptually. The same conceptual limitation in the model is there to distinguish family members that are engaged in social impact activities. The three-circle model can’t cleanly handle the distinction in general. But you can still make notations about a particular family’s three-circle map to indicate particular groupings of interests.

PS: I’ve always wondered if we could get away from two dimensions. If we could see some things in three dimensions that would be different or more powerful than what we currently seem capable of. In 2011, I was asked to speak on governance of a family and its enterprise at a conference in Taiwan. That’s the first time I used a three-sphere model as opposed to the three circles. I had all these different kinds of flowers and said, well, this is your family. These different flowers, some of them fading, others are in full bloom, and some are buds, etc., represent all the kinds of people in the family. Similarly, I used fish in a pond for another circle, and drops in an ocean for the third. So, we have the three circles and we have the seven regions, but even within the regions there are differences.

I think that more dimensions could offer some insights that we can’t appreciate now. I have drawn three spheres too but couldn’t get to new understandings through a three-dimensional representation. I think it would be cool to see a hologram where you could peer into the regions of each sphere and ask questions. Maybe we would appreciate the interconnections of the three systems better than we can today. I think there’s a richness in the model that we haven’t explored yet.

I’m so looking forward to getting to that stage in our thinking and practice! Where do you see us going? And where would you like us to slow down and take a moment to reflect on where we’ve been?

JD: It’s very impressive to me to see all the good thinkers and researchers who have discovered this field and are writing about it and having useful things to say. Right behind me in my office is my collection of FBR. Often, I find myself pulling out a specific year and looking to see what was written then. We’ve come a long way since 1984. I want researchers to understand the family business system to gauge how their particular research fits into the broad issues of the three-circle model. That takes extra effort on the part of researchers but I hope they do it. Research will be more useful if that happens.

FFI | Practitioner – June 6, 2018

To celebrate the 40th anniversary of the legendary Three-Circle Model, FFI Practitioner is excited to share two editions about the model during the month of June. For the first edition, we’d like to thank Pramodita Sharma for her interview about the inception and impact of the model on the field with one of its two creators, John Davis.

Pramodita Sharma (PS): What was the original idea behind the model? Has it been misused?

John Davis (JD): Well, remember that this framework came out very early in our interviewing of people who worked in family businesses. Most of them were family business leaders, many were founders, a few were later generation family member-employees. We needed a conceptual “place to put people” we were interviewing. We wanted to understand individuals’ viewpoints, their roles, their confusion about some topics, why certain decisions were difficult for them, and why they were dwelling on certain issues. Ultimately, we were trying to understand why individuals in these businesses (we didn’t call it a system yet) saw the world the way they did and what issues were important to them. The need to organize the information we were gathering and what we were learning led us to the three circles: the business, obviously; the family, naturally; but then, eventually, also the ownership group. Without accounting for the ownership group and perspective, we couldn’t bucket all the comments and data adequately. But with three circles, we could organize the information we were gathering and we thought, wow, the three-circle framework seems to be enough.

And it started as a framework. Frameworks are largely for bucketing information. Later, we saw that the three circles and the interaction of the three circles had great explanatory power, and we called it a model. A comprehensive, predictive theory of action and reaction in the family business system hasn’t been accomplished, and maybe won’t be developed given the many intervening variables that can affect the outcomes of certain changes in any circle.

The original intent of the three-circle model was to locate individuals in the system, identify their various interests, and observe how individual and group interests and behaviors interacted. The three circles can also indicate thematically, for example, that the goals of the three groups can overlap and still be distinct. The clarity and simplicity of the model allowed people in the field to explore many topics. It has guided our thinking in this field in fundamental ways. That’s all we needed in the beginning, and it has held up well, I would say.

When you build a framework or a model, you hope it helps you understand a lot, but soon enough you see that it doesn’t do everything. Advisers don’t have a clear place in the model. Governance structures, for example, with their adviser members, don’t fit perfectly in the geometry of the three circles. That said, non-purists can still add a board of director’s symbol in the overlap of business and ownership groups, and readers can see where it belongs in terms of its responsibilities.

As for examples of misuse, I can’t go that far. Some people thought highly enough of the three-circle model that in the early days they claimed it as their invention. But that’s different than misuse. Some have found the original three-circle model frustrating because it doesn’t do what they want it to do—like have clear categories for advisers or governance groups. I would add that the three-circle model doesn’t adequately diagram the situation of a multi-family business. But attempts to build a substitute model, with the necessary complexity to account for other memberships, haven’t been received well because they are either conceptually flawed or very complex and hard to use. I haven’t seen a workable (clear and relatively uncomplicated) four-circle model although it’s been tried.

I wouldn’t call these a misuse of the model, but it’s not how we initially thought of it. Sometimes to make a point, people will move the circles around, separate a couple of the circles, make circles of different size, etc. That’s a different use of three circles and it’s fine if it gets you someplace in your thinking and explanations. In general, I think people have used the model in ways that have been useful.

PS: Can you share the spirit of the conversations and thought processes you went through when this model was created? What was it like working with Ron Taguiri?

Cambridge Family Enterprise Press, 2018

A family business advisor sits with a founder and his two daughters in a conference room in Chicago, helping the family with an intense discussion they are having about the future of their family-owned brewery. The elder daughter works in the business. Neither daughter has shares in the family company. All three family members say they want what is best for the business and what is also fair to the three of them. But, for all of their agreement on principle, this discussion about future leadership, ownership and inheritance is getting testy and personal.

The advisor picks up a marker, goes to a flip chart, and begins to draw.

The circles he inscribes are a little wobbly, but that doesn’t matter. He labels the circles of the Venn diagram: Family, Ownership, and Business. He places each of the three family members in their appropriate sector of the diagram, and next to each of their names lists their interests and concerns. The diagram helps to clarify the roles and perspectives, and issues to be resolved.

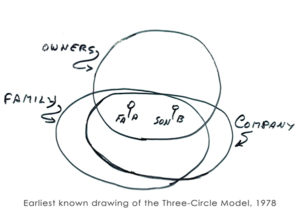

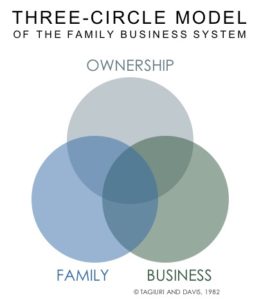

What the advisor has drawn is the Three-Circle Model of the Family Business System, the fundamental framework in the family business field, created by Renato Tagiuri and John Davis at Harvard Business School (HBS) in 1978.

Forty years ago, Tagiuri and Davis were looking for a framework to categorize the issues, interests and concerns they were hearing from Tagiuri’s executive students who led family companies. In 1978, Davis was a first-year doctoral student and Tagiuri, a senior professor of organizational behavior. Davis had a strong interest in family psychology as well as in business organizations. Tagiuri was a new faculty member in the Owner President Management (OPM) executive program at HBS, where most of the participants owned family companies. Tagiuri invited Davis to become his research assistant so they could both learn about family companies. It proved to be a very successful and enduring academic partnership that lasted over 30 years.

Over the next four and a half years, while Davis finished his doctorate, the duo conducted numerous interviews with family company owner-managers and surveyed hundreds of executive students on various family business topics. They met almost daily to discuss their projects and findings in the lounge of Humphrey House, Tagiuri’s office building on the Harvard Business School campus. They would take over the lounge for hours, spread their papers over the conference table, and discuss the latest survey or interview results.

“Renato would ask me, “What are we finding in this interview?” John Davis recalled. “I would explain the themes of the interview and the issues that I could spot. Then we would start diagramming the situation, trying to explain why this issue or that problem came about, and how the family influenced the business, and so on. Tagiuri drew circles, triangles, flow diagrams, and stick figures of fathers and sons (at that time there were few women in the OPM program, or in most family businesses).” Davis adopted diagramming as a way to express ideas, and continues to use this method to explain phenomena to students and colleagues. “We would go back and forth explaining whatever, and we came up with very solid understandings and some pretty wise recommendations for that time, like the need for governance to strengthen discipline among family members, although we didn’t call it governance back then.”

There was almost nothing in the literature to guide their exploration. Little had been written about any aspect of family businesses, and the only conceptual model of a family business system was a two-circle framework, which showed the family and the business as two overlapping systems or circles.

The Two-Circle Model recognized the influence of family and business on each other, and the need for alignment of family and business goals and interests. This model also made it easier to understand the confusion that individuals and the system could feel because of competing norms of the family and the business.

But for Tagiuri and Davis, even in the early stages of their work together, the two circles fell short of capturing the interactions and tensions they were seeing in the family business systems they were studying, from a fledgling retail operation owned and run by its husband-and-wife founders to a late generation manufacturing empire owned by cousins with many non-family executives.

So, they were on a hunt for a better framework. And it came several months after they began their research.

On this particular day in the fall of 1978, Davis reviewed a couple cases and Tagiuri took out his pen and drew two circles to represent the family and the business. “That’s part of it,” Davis remembers saying, “But in this system, they are fighting over getting shares in the company. Some of the family members are owners and some are not, and the two circles don’t account for that.”

Tagiuri thought for a moment. “Would this work?” he inquired, sketching out a third circle overlapping both of the first two, and labeling it Ownership.

“That’s it,” said Davis. “Some of these people are owners, some of them are family members, some are both. And some are also managers in the company. And this makes room for the people I am interviewing the most, the owner-presidents who are right in the center.”

Case by case, the pair started to work through specific family business cases to see whether these systems could be adequately described by the three circles. Husband and wife co-founders, Father-son companies, sibling partners, large cousin families with multiple branches, family managers actively running the business, owners and spouses who were not running the business, family employees who had not yet inherited ownership, young children in the family, relatives who had been bought out but were still in the family, non-family employees who were given minority shares, and even the anonymous public owners of listed family companies—all of them not only fit within the Three-Circle Model, their perspectives, goals, and concerns were better understood by it.

The addition of the third, ownership circle allowed more attention to be paid to other issues that were not explicitly recognized by the first two circles. Succession had to do with passing leadership and ownership. Some tough situations were resolved through buyouts of owners. Capitalizing a family business sometimes required bringing in outside owners. Linking the family, business, and ownership circles now fully defined the family business system, which is the integration of all three of these subsystems.

Elementary it may seem, but for forty years now academics, business families and their advisors have been sketching these three circles to gain insight into the inner workings of their family business and business family relationships. All family business systems can be described using the three circles, and each family business system can be uniquely understood with this framework.

It was this diagram (and the addition of the ownership circle) that also framed Tagiuri and Davis’s definition of family companies:

A family company is one whose ownership is controlled by a single family and where two or more family members significantly influence the direction and policies of the business, through their management positions, ownership rights, or family roles.

This definition could not have been derived without a three-circle perspective.

Three-Circle Model Explained

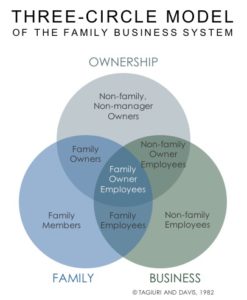

The Three-Circle Model of the Family Business System shows three interdependent and overlapping groups: family, ownership, and business.

An individual in a family business system occupies one of the seven sectors that are formed by these three overlapping circles. An owner (partner or shareholder) and only an owner will sit within the top circle. Family members will occupy the left-hand circle, and employees of the family company the right-hand circle. If you have only one of these roles, you will be in just one circle. However, if you have two roles, you will be in an overlapping sector, sitting within two circles at one time. If you are a family member who works in the business but has no ownership stake, you’re in the bottom-center sector. If you are a family member who works in the business and is an owner, then you will sit right in the center of the three overlapping circles.

“The Model identifies where key people are located in the system,” Davis explains, “and think about different roles that family members have: being a family owner, or a family employee. These overlap areas in the Model indicate role overlaps and potential role confusion.”

With the Three-Circle Model, one can depict seven distinct interest groups (or stakeholders) with a connection to the family business:

Each of the seven interest groups identified by the Model has its own viewpoints, goals, concerns, and dynamics. The Model reminds us that the views of each sector are legitimate and deserve to be respected. No one viewpoint is more legitimate than another but the different viewpoints must be integrated in order to set future direction for the family business system. The long-term success of family business systems depends on the functioning and mutual support of each of these groups.

Sitting around the conference table in Humphrey House lounge on the Harvard Business School campus in the late 1970s, Davis and Tagiuri had no sense that they were inventing a game-changer. For starters, there wasn’t really a game to be changed: the study of family business was in its infancy. “There was not only little writing on these systems, there was almost no conceptual thinking on these systems.” Davis explains.

Their intentions were very immediate and quite pragmatic: As they doodled, they were simply trying to develop a useful tool. “We just needed something convenient to be able to organize our thinking about how these systems were structured. That’s all we needed to do at first.”

From those doodles, though, came a model that allowed for deep analysis of family businesses, and led to benefits that are both direct and wide-ranging.

Here are six often-noted impacts and consequences of the use of the Three-Circle Model.

How One 5th Generation Family Conglomerate Used the Model

One 5th generation leader of a multi-billion dollar, family-owned conglomerate expressed the impact that the Model has had on his family’s understanding of their family business:

“A decade ago, we were in the midst of many challenges. Our values had become confused with our rules. Treating people with respect meant not firing anybody. Consensus meant that the scope for leadership was limited. Eventually these, and other issues, caused serious problems in the business. We had a governance crisis and a performance crisis, and closed one of our primary geographic regions’ operations.

That’s when we met John Davis, and the simple insight of the Three-Circle Model was revelatory. The fact that the circles are related but distinct, each with their own perspective, but linked, was illuminating. If one circle is unhealthy in its approach, it will affect the others. That was a significant shift for us.”

When so much in business, technology, wealth, family, and society has changed, how can a 40-year-old model still help us understand and manage issues in current family business systems?

Part of the reason why the Model has withstood the test of time, and is still relevant today, is that the Model, in its unaltered form, is adaptable. As the definition of “family” has changed in society, the Model allows for that. In-laws, blended families, divorce, adoption, domestic partners, and whoever the family calls a member of the “business family” because they are connected through ownership – all of these roles are consistent with the Model.

Likewise, the ownership circle can accommodate many possible scenarios. If a family business goes public or invites a private equity partner, the Model accommodates that ownership change. If the company issues different classes of stock (voting and non-voting), and holds some of the shares in a trust, the Model accommodates that. Today, as families have many different capital alternatives, the Model accommodates joint ventures, mergers, acquisitions, and different sources of capital that impact the ownership circle.

Many businesses have changed significantly in 40 years but the business circle of the Model is flexible: It may represent one business, or multiple businesses, holding companies, joint ventures and more. It can even describe a situation where the business family has sold its operating company and is managing their financial assets as an entity. The family is in a different business, but it is still their business. Similarly, the “business” circle can be labeled the “family office,” and the model still works.

With the pace of change, globalization, technological advancements, and disruption around the world, the changing environment will continue to shape businesses, ownership groups, and families. And the Three-Circle Model will continue to accommodate this evolution.

Like designing a three-wheeled car or adding a second story to an Eichler house, sometimes a classic design stays around because it simply can’t be improved on—given its purpose.

Over the years, many family business practitioners have sought to improve on the three circles. They have added more circles, and redrawn them as overlapping ovals. “Sometimes,” says Davis, “these models accomplish their purpose. But they tend to be complicated and not do as efficiently what the Three-Circle Model does.”

Davis himself has, over the years, tinkered with adaptations and additions to the three circles. “I played around for a while with the idea of having a fourth circle of wealth holders because in some situations the holders of family wealth differ from the owners of the family business. I wondered if we could try to map wealth holders distinct from owners. The fourth circle just didn’t work.”

Nothing seems to have the sticking power of the original Three-Circle Model. It is still the widely accepted, organizing framework used worldwide to understand family business systems. The acid test for the Three-Circle Model, Davis says, is this: “No one in the world now addressing family business issues doesn’t use it.”

Simplicity is central to the efficacy of the Three-Circle Model, Davis contends. “Models that have legs – that keep working – need to be simple enough to describe most of what you need to describe, and the Three-Circle Model does that.”

Expedient as it may be, even the Three-Circle Model has its limitations, and Davis is ready to concede that. “You know, it’s just a helpful tool and it’s not the only tool that you need.” He goes on to illustrate his point with another example. “We could describe your family business system using the Three-Circle Model. But your family also has a family vacation house, a family philanthropic foundation, financial investments that are managed collectively, maybe an art collection. All of these assets and activities influence one another and are important to your family but this collection isn’t captured by the Three-Circle Model. I created another framework for that, looking at the family enterprise system, which is a broader term than the family business system.”

So what lies in the future for the Three-Circle Model? Will we be using these same three circles in another forty years’ time?

“I think that the Model will still be the Model,” Davis says. “I think we will make more progress understanding how the family business system fits into the broader family enterprise system. I also think we will use the ability to map systems not in a two-dimensional way, but in a three-dimensional way. In my mind’s eye I can see three intersecting spheres and maybe being able to represent a family business system in three-dimensional space could allow some breakthroughs in understanding. But I don’t think somebody will come up with a fourth circle that compels people to do away with the three circles.”

The Three-Circle Model of the Family Business System was developed by Renato Tagiuri and John Davis at Harvard Business School, and circulated in working papers starting in 1978. It was first published in Davis’ doctoral dissertation, The Influence of Life Stages on Father-Son Work Relationships in Family Companies, in 1982. In 1996, the Family Business Review published it in Tagiuri and Davis’ classic article, “Bivalent Attributes of the Family Firm.”

_________________

Cambridge Family Enterprise Press, 2018

For permission to quote or distribute this article, contact [email protected]

Originally published in: Family Capital (October 12, 2017)

Dual-class stock listings, often favored by founders and families who take their companies public, have a bad rap with a number of stock markets, stock analysts and especially with institutional investors. These investment companies, including pension funds and other investment pools, claim dual-class systems are a threat to “democratic norms” in public markets because these ownership systems “entrench” families in control of their family companies. The business press has largely fallen in line with these critics, I think because they haven’t examined the benefits of dual-class systems and the weaknesses of today’s stock markets.

Dual-class stock structures are beneficial for the economy because they allow families to stay in control of their companies while holding just a minority of the economic value of the family company. In a dual-class system, the class of shares held by the controlling family gives the family more votes per share (sometimes even all the votes), or special rights, in order to elect the board of directors they want. This allows these publicly traded family companies to pursue long-term objectives insulated somewhat from the extreme short-term pressures of the stock market.

We should want all public companies to take actions that strengthen their long-term performance, like improving their operating efficiency and stimulating ongoing innovation, developing great managers and skilled employees, investing in promising new opportunities, and changing outmoded strategies and policies. These choices, however, usually require a long period to implement. Pressures that lead a company to avoid useful longer-term investments and changes so that short-term/quarterly results seem better, are wasteful and harmful to the economy and should be avoided.

It is widely acknowledged that public companies feel pressured to take short-term actions to demonstrate that their quarterly earnings meet the expectations of analysts and key investors. Public companies are even known to manipulate their financial statements in response to quarterly pressures on earnings to achieve desired short-term results. Institutional investors are the most influential actors producing this short-term orientation. If a company narrowly misses its quarterly projections, institutional investors can and do move mountains of investment capital from one company to another. Anonymously-owned public companies are most vulnerable to these pressures. Have you observed that especially anonymously–owned public companies have been hording mountains of cash, not investing it, or using it to buy back their own shares? A key reason for this is that long-term bets by a company generally don’t produce quick short-term gains to a company’s stock price and could depress the stock price for a period. Publicly traded single class family controlled companies do somewhat better at resisting short-term pressures because they naturally have a longer-term, sustainability orientation. Family companies with dual class ownership systems do the best of the lot.

To understand the short-term bias in the stock market just follow the money. The stock market’s focus on short term results agrees with the compensation incentives of many public company executives and institutional investor managers even if this bias perversely constrains the long-term performance of public companies. If you want change the orientation of public companies and institutional investors, change how their key managers are compensated.

This pressure by institutional investors on stock markets, in my opinion, constitutes a real threat to the health of capitalism because short-term pressures sway companies in the wrong direction. Marx warned us that economies and societies plant the seeds of their own destruction. Institutional investors — a natural outgrowth of large stockpiles of investment capital combined with investment managers with a mentality (encouraged by their compensation system) to maximize short-term economic gains are these seeds.

Democratic norms in a public stock market do not mean that all owners have the same votes, as institutional investors have cleverly skewed the debate to argue. Public markets should be democratic in this way: public companies need to be responsible, clear about their strategies (long-term, short-term, etc.), and transparent enough for investors to know how they are really performing against their stated strategies. Individual investors in the stock market come in all flavors—short-term and long-term oriented, some wanting liquidity, others appreciation. Public markets should make it easy for investors to know what they are buying. If stockholders don’t like what a public company is doing, they can vote with their feet. If public companies cheat stockholders, regulators should catch them and punish them. We need regulations and laws that promote good corporate behavior. A good board will help a company perform better for all owners, given its stated strategy. Having an ownership control group in place helps to choose a board that can help a company be responsible and achieve long-term success.

I think that public stock markets can serve a good purpose. We need to have a diverse ecology of mechanisms in an economy to capitalize companies (debt, private equity, public ownership, etc.), including a public market option that serves all companies well and flexibly. Public markets have their obvious costs for companies, including transparency and compliance costs. The big problem comes from institutional investors. Because many institutional investors have relatively big positions in public companies, they can be very disruptive in the wrong way. The short-termism of institutional investors is what I really object to. Public markets need to wake up to the threat of powerful, short-term investors. Public ownership has already become less and less attractive to companies, and stock markets are shrinking. They will shrink more if they restrict dual-class shares. The stock markets shouldn’t let institutional investors be the seeds that undermine the value that stock markets can have.

Originally published in: Huffington Post (July 25, 2017)

The pictures of Jared Kushner and Ivanka Trump participating in executive and ceremonial meetings with foreign leaders draw the ire of many. These images raise central questions about the legitimacy and utility of nepotism in the White House.

Most commentators regard the governmental presence of Kushner-Trump as, at the minimum, overstepping the proper roles of relatives supporting their family leader. More critically, their presence is a poor and inappropriate substitute for professionals who should be in these advisory roles. The most generous comment I have read about the Trump scions’ administrative roles is that they seem to have a moderating influence on the President and, therefore can help him perform better. However, in face of recent news about the practices and approaches engaged in by his children, this theory no longer seems credible.

Do Ivanka Trump and Jared Kushner belong in these roles? This is a central question for my field of family business management, as we witness the U.S. president attempt to run the White House in the same manner as his family businesses. They have the confidence of President Trump, who indicates that he is proud of his daughter and son in-law, and trusts them to represent and advise him on both foreign and domestic issues. Despite the fact that they have achieved some success—in their respective businesses—Ivanka Trump and Jared Kushner do not have experience or demonstrated skills that would qualify them for their roles in the current administration.

“In their respective businesses” is an important clause and underscores why we are justified in labeling Trump-Kushner as harmful nepots. The term nepotism is associated with giving preference in hiring and promotion to one’s relatives, independent of their merit or qualifications. To be fair, all species — from single-cell organisms to orangutans to humans — favor their close relatives, granting them more care, resources and opportunities. Most people (probably including you, dear reader) probably support and sympathize with a family’s desire to favor passing its assets to succeeding generations, as in a family company.

Assuming that President Trump views them as qualified for their posts (remembering that he views himself as highly qualified for his current position), we must still recognize that he chose them, in particular, because he wanted family members in his advisory team. He favored them in government employment because of their family membership and loyalty to him, not for their professional and governmental acumen. Hence, they are harmful nepots – instead of “nepotistic professionals,” family members who are qualified to serve in specific roles.

Professionals are individuals who, emphasizing the latest tools of their crafts, exhibit high standards of performance and ethics. Professional behavior can be seen (or not) in both family and non-family employee groups. The fact that Jared and Ivanka are family members does not automatically mean they are not professionals. Their lack of governmental and topical experience means that they are not nepotistic professionals either. For anyone to be a professional means that he or she is schooled, trained and has developed the understandings, skills and ethics of one’s trade and is qualified to be in a particular position – which Trump and Kushner are not.

President Trump, who behaves as if he and his family own the White House, has trampled on the principle of nepotistic professionalism by installing his daughter and son in-law in roles they are clearly not prepared for. In doing so, he and they not only recklessly risk the performance of our government, but also damage the image of their family and of family companies overall.

Dr. John A. Davis is a globally-recognized authority, academic and researcher on family business and family wealth. Learn more about Dr. Davis at johndavis.com, on Twitter at @ProfJohnDavis, and on LinkedIn.

Originally published in: Family Capital (August 24, 2016)

Photo: Pixabay

Perhaps the most challenging issue for China’s private businesses in the years ahead is how they deal with succession. Given the country’s brief 30 year experience with a market economy, China’s family businesses have yet to fully embrace succession. That, of course, is changing – as the founder generation begins to transition to the second generation. But what is becoming increasingly clear is that China wants to shape its own thinking on succession, which borrows ideas from the west, but is also about something that feels distinct for themselves.

At many levels, passing the business to the next generation is no different for family-owned businesses in China than it is for other family businesses anywhere else. They face the same set of challenges, such as getting the next generation prepared and committed to taking over management plus encouraging the senior generation to let go in time. The ultimate goal, for any business, is to maintain both the momentum of the business and the family. That’s no different for China’s family businesses.

But succession in China has some particular twists. One of these is that the country is largely dealing with founder succession. Of course, issues around founder succession are universal, where the founder has an intense attachment to the company and they fear to let go.

“China is largely dealing with founder succession”

But the founder generation is split in China between older Phase 1 founders who started in the 1980s and early 1990s, and younger Phase 2 founders who launched private companies in the late 1990s and 2000s. The older Phase 1 founders are mostly in their 70s now, and were mostly involved in transforming state enterprises that weren’t doing very well into private enterprises; they were part of the state structure and their thinking has been influenced by that culture. The younger Phase 2 founders, who are mostly in their 50s, started their own companies from zero and are more similar to the entrepreneurs in the west.

It is the older founders that currently face the greatest challenge with succession, for three predominant reasons.

Because of China’s one-child policy, the family does not really have a choice in terms of who they appoint as their successor. This is especially true because China has yet to develop a deep pool of professional, non-family, senior management talent that operates with high ethics and can be trusted by family owners.

There tends to be a cultural gap between the senior and junior generation family members. Unfortunately, many next generation family members do not want to work in the family business. They often see the family business, usually connected to manufacturing, as unattractive because of the low growth of these industries, the often remote locations of production facilities, and the complexity of building and maintaining government relationships. Those feelings tend to be amplified if the next generation is educated abroad. The two generations diverge on their approaches to the family’s wealth strategy, business strategy for specific operating companies, and management strategy of how to lead the business organization effectively.

Another issue that often complicates succession in China is the concept of the extended family. Many times the founder supports members of the extended family informally. Sometimes this means giving relatives jobs inside the company or supporting them in their own business ventures. Typically, in China, the family is a significant obligation and becomes a real headache for the second generation, because they can’t fire members of the extended family working in the company. They also find it difficult to decrease other types of financial support over time, so they have to keep supporting them. This becomes an increasing burden as the size of the extended family grows in successive generations.

“In the west, the boundaries of a business family are its owners, their spouses and their immediate descendants; but in China, this idea almost feels socially unacceptable.”

This is further complicated by the fact that it often becomes difficult to define what is the boundary of the business family in China. In the west, it’s the owners, their spouses and their immediate descendants; but in China, this idea almost feels socially unacceptable. They see the business family as much broader, and this places a lot of pressure on the only child when it comes to managing expectations.

As a next generation family business cohort, it is uncertain whether generational transitions within Chinese family companies will generally be successful since succession has yet to go through a whole cycle, which will probably occur in 15 to 20 years time. There have been a few successful cases of family business generational transitions in China so far. For example, Liu Yonghao who founded one of the largest private agribusinesses in China—New Hope Liuhe Co—ceded the chairmanship of his company to his 33-year old daughter Liu Chang in 2013 when he was 62 years old. He selected a director on the company board to be the co-chairman with his daughter. Examples from places like Hong Kong and Taiwan, where succession often has not been well managed, are difficult to be held up as role models in China.

They will not just want to run their businesses as capitalist organizations, but adapt them to a Confucian way of thinking.Over time, it is our view that China is going to develop a succession strategy that is successful, and works for its huge economy—probably a more successful succession strategy than currently works in Hong Kong and Taiwan. But to get there, China still needs to confront a number of challenges—and many of these go to the heart of what type of society China sees itself as.

Originally published in Harvard Business School: Working Knowledge (Sept 4, 2001)

The topic of governance is hot. Shareholders, managers, and business advisors are demanding improved governance of (typically public) companies by strengthening their boards of directors and developing more responsive shareholder relations.

But what happens when your board of directors is also your family?

The governance of a family business is more complicated than for non-family owned companies because of the central role of the family that owns and typically leads the business. In a family business, the business, the family, and the ownership group all need governance.

In family businesses (companies whose ownership is controlled by a single family) and other kinds of family enterprises including family foundations and family investment funds, the lack of effective governance is a major cause of organizational problems. In my two decades of working with family enterprises of all kinds, it has been clear that every business able to improve governance reaped lasting benefits.

If you are in a family enterprise, you need to learn the basics of governance and apply the best practices that exist in family business governance. But even non-family business leaders can benefit from considering how the problems of a family enterprise and non-family business are often the same. Personalities, passions, and power, after all, are at the heart of any enterprise.

In this article, I will describe effective overall governance of a family enterprise. In the following two articles in this series I will go into more detail explaining governance of the family business and governance of the business family—the family that owns the enterprise.

Let’s start by defining our topic. For any organization, be it a business, a family, a family foundation, or a Boy Scout troop, effective governance:

No organization is effective for long without doing these things. You should measure the effectiveness of your governance system by these outcomes, not by the boards and councils you can put in place. Effective governance can be done in an informal, casual manner. Or it might require formal structures (e.g. boards, councils) and processes (e.g. agendas, voting). The particular kinds of structures in your governance system can vary as long as your organization is producing the two outcomes described above.

If your organization is doing the above two activities in an informal, casual way, don’t change. But if your organization does not have these outcomes—a clear sense of direction, clear values, well-understood, sensible policies, does not assemble the right people in a timely way to discuss and decide the big issues facing your organization—then your governance system is flawed, should be improved, and probably needs to be made more formal. Given how difficult it is for most people to confront especially sensitive issues and to plan ahead, some degree of formality often helps people focus on their issues, work toward their goals, and resolve their differences. What is clear in my work with family enterprises is that a few well-composed and well-managed governance structures greatly help your chances of being effectively governed.

The world of family enterprise generates a mixture of business, family and ownership concerns that can make these systems emotionally charged environments for planning and problem solving. In these systems individuals must manage issues within and across three overlapping groups: the family, the business, and the ownership group (see Figure 1). The overlap among the three groups often leads to differing points of view among individuals depending on their location in the three circles. For example, family shareholders not employed in the business often have different views about the proper level of dividends than do their relative owners who work in the business. Both viewpoints are typically legitimate and must be reconciled in a respectful way to set direction for the enterprise and preserve harmony in the family. To effectively manage business, family and ownership concerns requires communication and decision making within and across the family, the business, and the ownership groups.

The overlap among the three groups often leads to differing points of view among individuals depending on their location in the three circles. For example, family shareholders not employed in the business often have different views about the proper level of dividends than do their relative owners who work in the business. Both viewpoints are typically legitimate and must be reconciled in a respectful way to set direction for the enterprise and preserve harmony in the family. To effectively manage business, family and ownership concerns requires communication and decision making within and across the family, the business, and the ownership groups.

Figure 1: The “3-circle” model of family business

Without belaboring an oft-made point about family business, reconciling these diverse concerns can be terribly difficult. Too often, family firms employ dysfunctional and short-sighted approaches to handle tensions, such as:

These methods of addressing business-family-ownership tensions can provide some short-term relief but rarely resolve issues and predictably intensify them. Effective governance does not eliminate tensions in family enterprise systems. But it can reduce tensions and improve the effectiveness and harmony of these systems by clarifying family-business-ownership needs and managing the conversations needed to agree on goals, values, and policies.

“IF YOU ARE IN A FAMILY ENTERPRISE, YOU NEED TO LEARN THE BASICS OF GOVERNANCE AND APPLY THE BEST PRACTICES THAT EXIST IN FAMILY BUSINESS GOVERNANCE.”

— JOHN DAVIS

The absence of effective governance is by no means confined to smaller companies. The board of a large, fourth-generation family company created painful family turmoil when it dismissed the family chairman. The dismissal seemed abrupt to the chairman and his family allies, and long overdue by others. The family had the wisdom to address the ensuing family conflict and expose the weaknesses of its existing governance system: the family council was not consulted about the board’s issues with the chairman and did not understand its role in working with the board on such issues; the board of directors was too dominated by the family which had kept it paralyzed and unable to give the chairman pointed, critical feedback. This family business had the right structures in place; they just weren’t working properly. By strengthening the board and family council, and using the board, council, and family assembly to confront real issues facing the family and business, the business and most of the family moved beyond the removal of the chairman. They were also able to begin addressing the exclusion and secrecy at the root of problems in their system. This family business sold two of its three companies; the family is making a real attempt to become more supportive and cooperative. The improved governance system was at the heart of both gains.

Good governance contributes three fundamental ingredients for family businesses to function well:

So far, we have established the philosophy underpinning family business governance. Now, let’s review the structures in a family business governance system. Effective governance requires forums for the examination of the complicated and often emotional family, business, and ownership issues that confront family firms. The structures I recommend for any family-business-ownership system will vary somewhat based on the size and diversity of the business organization, the size and diversity of the ownership group, and the size, generation, and diversity of the family. One type of governance structure does not fit all family enterprise systems. But most family enterprise systems can be governed by a few structures, shown in Figure 2:

Figure 2: Basic governance structures of the family business system

The membership and functions of these governance structures need to evolve as the business, family, and ownership groups change over time. A first-generation family business may only require (or tolerate) a small, informal advisory board rather than a board of directors. A third-generation family may need a family assembly to bring together the twenty-two members of the family annually to learn about and discuss the family business, plus a family council to help set policy for the family. It is quite clear that as ownership of the family business becomes more divided over generations, board composition and the role of the family council need to change. My advice is to create your board, family council, or family assembly to meet your current needs and to periodically discuss how to update these structures to meet the needs of your changing system.

The relationships among the governance structures is depicted in Figure 3 below:

Figure 3: Relationships among governance structures

This diagram illustrates the principle of the separate functions of the family council and the board of directors, or “the separation of church and state.” The family council sets policy for the family and recommends policy that concerns the family to the board (e.g. policy about family employment in the business). The board of directors sets policy for the business and may also make recommendations to the family council in matters that concern the business. These board and family council will ideally coordinate their work (we will discuss how later) but they should not overstep into each other’s domains.

At this point, consider my description of effective governance and assess how well your family enterprise performs according to the standards I have proposed. Then ask if your family enterprise system might be helped by a formal structure or two.